Everyone knows that finance and accounting deals with money. What they don't know is that these two subjects are not black and white. Assuming ethical behavior is taking place, there are three factors that make the numbers not so obvious, predictable, or in other words, black and white.

First, the interpretation of many measurements can vary because there is not a globally accepted way to calculate everything. Not only are there different accounting standards from country to country, the best way to calculate many financial ratios differs depending on who you talk to. There are also different algorithms to calculate items such as depreciation and inventory attributes. Knowing the general theory behind many financial ratios can lead to a more correct interpretation.

Second, assumptions are used to predict elements that are unknown. These assumptions are best guesses by individuals that themselves may not have all relevant information. Aside from discussions or critical thinking, assumptions can also come from a probability analysis based on best and worst case outcomes. A common simulation used to create these assumptions is the Monte Carlo method.

Third, the availability of inside information may not be widely known, but may contribute significantly to changes in the numbers. This factor can be hedged by having an understanding of annual and quarterly reports. One of the most important parts of annual and quarterly reports, besides the actual financial statements, is the Management Discussion and Analysis (MD&A). Management is required to divulge any important risks, benefits, or other factors that could affect the current state of the company or any official projections that have been made.

Show Me the (Real) Money

There are several things that everyone should know about a company in terms of its finances. The most important aspect of a company's finances is usually all about valuation.

Many people think of stock price as the major financial indicator for how a company is doing at the minute. In reality, stock price is a supply and demand for a share of a company that represents all future profits and growth. It's valuation.

Valuation has many facets which include relative comparisons to industry averages. It also includes cash flow, sustainable growth (internal and external), and general ratio analysis. Although there are macro economic factors like substitute products that can affect a company's value, most of the elements that a company can control are embedded in their financial statements.

Financial statements are required for publicly held companies and usually take the form of 10-Q and 10-K filings. There are other filings for non US-based companies, but they are very similar to the 10-Q/K statements. While there are also 8-K statements that show important changes and announcements a company is making, 10-Q/K statements show the major financial statements and other important information about the company. The 10-Q/K statements are created on a quarterly (Q) and annual (K) basis.

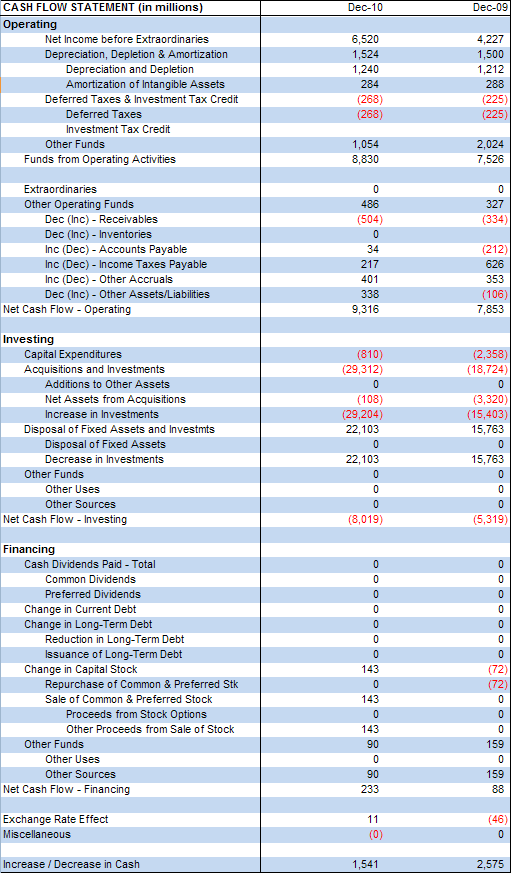

The major financial statements included in 10-Q/K filings are the Income Statement (Profit and Loss or P&L), the Balance Sheet (Statement of Financial Position), and the Statement of Cash Flows. Each of these statements has its own purpose, but interacts heavily with the others.

For each statement, there is a general accounting equation that describes the content:

Example Balance Sheet

Example Cash Flow Statement

There are many more ratios, but these are used quite a bit. There are expansions on ratios such as P/E -> PEG. One additional expansion ratio not previously mentioned that does carry some fame is the DuPont expansion of ROE. Its purpose is to give a better idea of what contributes to ROE by showing that ROE can be expanded to three separate other ratios if identical numerator/denominator pairs are not canceled out:

It is important to note that while the theory of each financial ratio is generally the same, they are sometimes calculated differently and must be compared only to other ratios that have been calculated in the same manner.

Again, it is important to stress that when making numeric comparisons, things are calculated in the same way. Use the numbers, management comments, and any other information you have, but remember that you will ultimately be making decisions based on this information and you must both understand it and take it with a grain of salt. Everyone ends up having their own interpretation.

Many people think of stock price as the major financial indicator for how a company is doing at the minute. In reality, stock price is a supply and demand for a share of a company that represents all future profits and growth. It's valuation.

Valuation has many facets which include relative comparisons to industry averages. It also includes cash flow, sustainable growth (internal and external), and general ratio analysis. Although there are macro economic factors like substitute products that can affect a company's value, most of the elements that a company can control are embedded in their financial statements.

Financial statements are required for publicly held companies and usually take the form of 10-Q and 10-K filings. There are other filings for non US-based companies, but they are very similar to the 10-Q/K statements. While there are also 8-K statements that show important changes and announcements a company is making, 10-Q/K statements show the major financial statements and other important information about the company. The 10-Q/K statements are created on a quarterly (Q) and annual (K) basis.

The major financial statements included in 10-Q/K filings are the Income Statement (Profit and Loss or P&L), the Balance Sheet (Statement of Financial Position), and the Statement of Cash Flows. Each of these statements has its own purpose, but interacts heavily with the others.

For each statement, there is a general accounting equation that describes the content:

- Income Statement: Revenues - Expenses = Profit/Loss

- Balance Sheet: Assets = Liabilities + Shareholder's Equity

- Statement of Cash Flows: Operating Cash + Investing Cash + Financing Cash + Beginning Cash = Ending Cash

Example Income Statement

Example Balance Sheet

Example Cash Flow Statement

Financial Ratios are created from line items of the three financial statements previously mentioned. They can be grouped into six categories:

Liquidity

Ratio calculation- Current Ratio

- Quick Ratio

- Debt to Equity Ratio

- Receivables Turnover

- Fixed Asset Turnover

- Total Asset Turnover

- Days of Sales Outstanding (DSO)

- Debt Ratio

- Times Interest Earned (T.I.E.) Ratio

- Fixed Charge Coverage Ratio

- Net Profit Margin

- Return on Assets (ROA)

- Return on Equity (ROE)

- Price to Earnings (P/E) Ratio

- Cash Flow per Share Ratio

- Book Value per Share Ratio

- Market to Book Ratio

- Economic Value Added (EVA)

- Market Value Added (MVA)

- Internal Growth Rate (IGR)

- Sustainable Growth Rate (SGR)

- Price-to-Earnings to Growth (PEG) Ratio

There are many more ratios, but these are used quite a bit. There are expansions on ratios such as P/E -> PEG. One additional expansion ratio not previously mentioned that does carry some fame is the DuPont expansion of ROE. Its purpose is to give a better idea of what contributes to ROE by showing that ROE can be expanded to three separate other ratios if identical numerator/denominator pairs are not canceled out:

It is important to note that while the theory of each financial ratio is generally the same, they are sometimes calculated differently and must be compared only to other ratios that have been calculated in the same manner.

A company comparison using ratios

Again, it is important to stress that when making numeric comparisons, things are calculated in the same way. Use the numbers, management comments, and any other information you have, but remember that you will ultimately be making decisions based on this information and you must both understand it and take it with a grain of salt. Everyone ends up having their own interpretation.

Strategy Performance Part II 09 December, 2010

Even though most people are concerned about their own health, I'm guessing that a small percentage of those people don't really think about the health of the company they work for. I would argue that although many employees are constantly searching for that next innovation, simple process improvement would improve the average company just as much.

Process improvement is not only about improving, it's also about knowing what is possible. A process is working well if it consistently performs well, and has a low level of daily variance. When looking at a company checkup in terms of its process health, the investment in improvement is not as expensive as first impressions may indicate. In fact, many studies show that it is not the willingness or ability to improve, but the time required that is often the problem.

Four main goals of process improvement are:

Two popular ways of improving processes are benchmarking and waste identification. Either way, it's all about removing things that do not add value and adding more value where it is needed.

Benchmarking is all about using metrics to grade a process. These grades can then be compared to either other internal benchmark grades or external benchmark grades dealing with similar processes. Internal comparisons are used for continuous improvement from where the company was previously at. External comparisons are used to find out how well a process compares to the best versions of those processes on a local, national, or even global scale.

Benchmarking and process improvement is comprised of the following steps:

Cause and Effect diagrams are useful for finding root causes to problems. Looking at the following diagram, you can see why some people call it a fishbone diagram. Every time there is a reason for the effect, an attempt is made to find a lower level cause.

Pareto charts are cross plots of specific problem types vs total problems (relative vs. absolute). They are useful in showing which problem areas should be addressed first.

If it is uncertain whether a process needs to be benchmarked or improved, try looking at that process from a customer's perspective and see if you would be impressed or left wanting.

Process improvement is not only about improving, it's also about knowing what is possible. A process is working well if it consistently performs well, and has a low level of daily variance. When looking at a company checkup in terms of its process health, the investment in improvement is not as expensive as first impressions may indicate. In fact, many studies show that it is not the willingness or ability to improve, but the time required that is often the problem.

Four main goals of process improvement are:

- Cutting costs

- Cutting waste

- Improving quality

- Removing stress

Two popular ways of improving processes are benchmarking and waste identification. Either way, it's all about removing things that do not add value and adding more value where it is needed.

Benchmarking is all about using metrics to grade a process. These grades can then be compared to either other internal benchmark grades or external benchmark grades dealing with similar processes. Internal comparisons are used for continuous improvement from where the company was previously at. External comparisons are used to find out how well a process compares to the best versions of those processes on a local, national, or even global scale.

Benchmarking and process improvement is comprised of the following steps:

- Talk to those dealing with the process (to gain information and buy-in)

- Create metrics for comparing improvement levels

- Collect metrics before a change (as the process exists today)

- Make the change

- Collect metrics after a change

- Make sure the improvements and measurements are statistically significant

- Present findings, real world benefits, and recommendations

- Officially incorporate the changes into the process

- When needed, benchmark again for continued improvement

- Time

- Number of people involved

- Number of manual steps

- Number of communication methods or problems

- Amount of redundancy

- Transportation (moving things more than needed)

- Inventory (any unneeded storage or depreciation)

- Motion (people moving more than needed)

- Waiting

- Over production (making more than needed)

- Over processing (poor tool use)

- Defects (taking extra time to find defects and fix them)

- Underutilized resources

- Process Diagrams & Value Stream Mapping

- Cause and Effect (also known as either Fishbone or Ishikawa diagrams)

- Pareto Charts / Analysis

Cause and Effect diagrams are useful for finding root causes to problems. Looking at the following diagram, you can see why some people call it a fishbone diagram. Every time there is a reason for the effect, an attempt is made to find a lower level cause.

Pareto charts are cross plots of specific problem types vs total problems (relative vs. absolute). They are useful in showing which problem areas should be addressed first.

If it is uncertain whether a process needs to be benchmarked or improved, try looking at that process from a customer's perspective and see if you would be impressed or left wanting.

Strategy Performance 07 December, 2010

After strategies have been created and a direction has been set, a company must perform well to see the desired results. One popular way to measure strategy performance is by using a Balanced Scorecard (BSC).

The BSC was popularized by Robert Kaplan and David Nortan in 1992. It is similar to a dashboard, but with a focus on company and consumer trade-offs. Stress is placed on an informing purpose rather than a controlling one. It can be thought of as a way to measure strategy because it links a company's actions to its mission and vision.

Balanced Scorecards are created based on four quadrants:

Each of these quadrants are further broken down into:

Goals should be specific, but cover many parts of each quadrant such as:

There are many benefits to the BSC which include:

The BSC was popularized by Robert Kaplan and David Nortan in 1992. It is similar to a dashboard, but with a focus on company and consumer trade-offs. Stress is placed on an informing purpose rather than a controlling one. It can be thought of as a way to measure strategy because it links a company's actions to its mission and vision.

Balanced Scorecards are created based on four quadrants:

- Internal Processes (how efficient are you at satisfying customers?)

- Customers (how do customers see you?)

- Finances (how do shareholders see you?)

- Internal Learning and Innovation (how can you create more value?)

Each of these quadrants are further broken down into:

- Goals

- Measurements

Goals should be specific, but cover many parts of each quadrant such as:

- Short/Long Term

- Financial/Non-Financial

- Leading/Lagging Indicators

- Internal/External Indicators

The following flow shows how the BSC connects strategy to action.

There are many benefits to the BSC which include:

- Showing the impact one change has on other quadrants

- The ability to measure intangible assets

- People are pulled towards the company mission and vision

- Areas that seem disjoint, but are linked, are identified

- Everyone in the company is involved

- Cause and effect relationships between BSC goals and outcomes are identified

- It shows which changes are reflected in the bottom line

- Goals should always be linked to the strategy

- Cause and effect relationships between goals and outcomes should be validated

- Measurements must be valid and statistically significant

- The goals should be communicated throughout the entire company

- Time should be taken to understand how quadrants and quadrant goals are related

Subscribe to:

Posts (Atom)