Everyone knows that finance and accounting deals with money. What they don't know is that these two subjects are not black and white. Assuming ethical behavior is taking place, there are three factors that make the numbers not so obvious, predictable, or in other words, black and white.

First, the interpretation of many measurements can vary because there is not a globally accepted way to calculate everything. Not only are there different accounting standards from country to country, the best way to calculate many financial ratios differs depending on who you talk to. There are also different algorithms to calculate items such as depreciation and inventory attributes. Knowing the general theory behind many financial ratios can lead to a more correct interpretation.

Second, assumptions are used to predict elements that are unknown. These assumptions are best guesses by individuals that themselves may not have all relevant information. Aside from discussions or critical thinking, assumptions can also come from a probability analysis based on best and worst case outcomes. A common simulation used to create these assumptions is the Monte Carlo method.

Third, the availability of inside information may not be widely known, but may contribute significantly to changes in the numbers. This factor can be hedged by having an understanding of annual and quarterly reports. One of the most important parts of annual and quarterly reports, besides the actual financial statements, is the Management Discussion and Analysis (MD&A). Management is required to divulge any important risks, benefits, or other factors that could affect the current state of the company or any official projections that have been made.

Show Me the (Real) Money

There are several things that everyone should know about a company in terms of its finances. The most important aspect of a company's finances is usually all about valuation.

Many people think of stock price as the major financial indicator for how a company is doing at the minute. In reality, stock price is a supply and demand for a share of a company that represents all future profits and growth. It's valuation.

Valuation has many facets which include relative comparisons to industry averages. It also includes cash flow, sustainable growth (internal and external), and general ratio analysis. Although there are macro economic factors like substitute products that can affect a company's value, most of the elements that a company can control are embedded in their financial statements.

Financial statements are required for publicly held companies and usually take the form of 10-Q and 10-K filings. There are other filings for non US-based companies, but they are very similar to the 10-Q/K statements. While there are also 8-K statements that show important changes and announcements a company is making, 10-Q/K statements show the major financial statements and other important information about the company. The 10-Q/K statements are created on a quarterly (Q) and annual (K) basis.

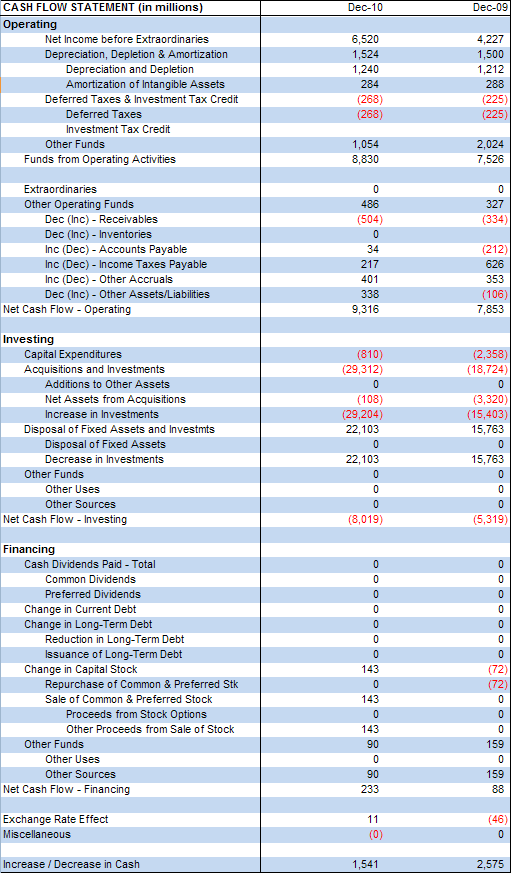

The major financial statements included in 10-Q/K filings are the Income Statement (Profit and Loss or P&L), the Balance Sheet (Statement of Financial Position), and the Statement of Cash Flows. Each of these statements has its own purpose, but interacts heavily with the others.

For each statement, there is a general accounting equation that describes the content:

Example Balance Sheet

Example Cash Flow Statement

There are many more ratios, but these are used quite a bit. There are expansions on ratios such as P/E -> PEG. One additional expansion ratio not previously mentioned that does carry some fame is the DuPont expansion of ROE. Its purpose is to give a better idea of what contributes to ROE by showing that ROE can be expanded to three separate other ratios if identical numerator/denominator pairs are not canceled out:

It is important to note that while the theory of each financial ratio is generally the same, they are sometimes calculated differently and must be compared only to other ratios that have been calculated in the same manner.

Again, it is important to stress that when making numeric comparisons, things are calculated in the same way. Use the numbers, management comments, and any other information you have, but remember that you will ultimately be making decisions based on this information and you must both understand it and take it with a grain of salt. Everyone ends up having their own interpretation.

Many people think of stock price as the major financial indicator for how a company is doing at the minute. In reality, stock price is a supply and demand for a share of a company that represents all future profits and growth. It's valuation.

Valuation has many facets which include relative comparisons to industry averages. It also includes cash flow, sustainable growth (internal and external), and general ratio analysis. Although there are macro economic factors like substitute products that can affect a company's value, most of the elements that a company can control are embedded in their financial statements.

Financial statements are required for publicly held companies and usually take the form of 10-Q and 10-K filings. There are other filings for non US-based companies, but they are very similar to the 10-Q/K statements. While there are also 8-K statements that show important changes and announcements a company is making, 10-Q/K statements show the major financial statements and other important information about the company. The 10-Q/K statements are created on a quarterly (Q) and annual (K) basis.

The major financial statements included in 10-Q/K filings are the Income Statement (Profit and Loss or P&L), the Balance Sheet (Statement of Financial Position), and the Statement of Cash Flows. Each of these statements has its own purpose, but interacts heavily with the others.

For each statement, there is a general accounting equation that describes the content:

- Income Statement: Revenues - Expenses = Profit/Loss

- Balance Sheet: Assets = Liabilities + Shareholder's Equity

- Statement of Cash Flows: Operating Cash + Investing Cash + Financing Cash + Beginning Cash = Ending Cash

Example Income Statement

Example Balance Sheet

Example Cash Flow Statement

Financial Ratios are created from line items of the three financial statements previously mentioned. They can be grouped into six categories:

Liquidity

Ratio calculation- Current Ratio

- Quick Ratio

- Debt to Equity Ratio

- Receivables Turnover

- Fixed Asset Turnover

- Total Asset Turnover

- Days of Sales Outstanding (DSO)

- Debt Ratio

- Times Interest Earned (T.I.E.) Ratio

- Fixed Charge Coverage Ratio

- Net Profit Margin

- Return on Assets (ROA)

- Return on Equity (ROE)

- Price to Earnings (P/E) Ratio

- Cash Flow per Share Ratio

- Book Value per Share Ratio

- Market to Book Ratio

- Economic Value Added (EVA)

- Market Value Added (MVA)

- Internal Growth Rate (IGR)

- Sustainable Growth Rate (SGR)

- Price-to-Earnings to Growth (PEG) Ratio

There are many more ratios, but these are used quite a bit. There are expansions on ratios such as P/E -> PEG. One additional expansion ratio not previously mentioned that does carry some fame is the DuPont expansion of ROE. Its purpose is to give a better idea of what contributes to ROE by showing that ROE can be expanded to three separate other ratios if identical numerator/denominator pairs are not canceled out:

It is important to note that while the theory of each financial ratio is generally the same, they are sometimes calculated differently and must be compared only to other ratios that have been calculated in the same manner.

A company comparison using ratios

Again, it is important to stress that when making numeric comparisons, things are calculated in the same way. Use the numbers, management comments, and any other information you have, but remember that you will ultimately be making decisions based on this information and you must both understand it and take it with a grain of salt. Everyone ends up having their own interpretation.

Strategy Performance Part II 09 December, 2010

Even though most people are concerned about their own health, I'm guessing that a small percentage of those people don't really think about the health of the company they work for. I would argue that although many employees are constantly searching for that next innovation, simple process improvement would improve the average company just as much.

Process improvement is not only about improving, it's also about knowing what is possible. A process is working well if it consistently performs well, and has a low level of daily variance. When looking at a company checkup in terms of its process health, the investment in improvement is not as expensive as first impressions may indicate. In fact, many studies show that it is not the willingness or ability to improve, but the time required that is often the problem.

Four main goals of process improvement are:

Two popular ways of improving processes are benchmarking and waste identification. Either way, it's all about removing things that do not add value and adding more value where it is needed.

Benchmarking is all about using metrics to grade a process. These grades can then be compared to either other internal benchmark grades or external benchmark grades dealing with similar processes. Internal comparisons are used for continuous improvement from where the company was previously at. External comparisons are used to find out how well a process compares to the best versions of those processes on a local, national, or even global scale.

Benchmarking and process improvement is comprised of the following steps:

Cause and Effect diagrams are useful for finding root causes to problems. Looking at the following diagram, you can see why some people call it a fishbone diagram. Every time there is a reason for the effect, an attempt is made to find a lower level cause.

Pareto charts are cross plots of specific problem types vs total problems (relative vs. absolute). They are useful in showing which problem areas should be addressed first.

If it is uncertain whether a process needs to be benchmarked or improved, try looking at that process from a customer's perspective and see if you would be impressed or left wanting.

Process improvement is not only about improving, it's also about knowing what is possible. A process is working well if it consistently performs well, and has a low level of daily variance. When looking at a company checkup in terms of its process health, the investment in improvement is not as expensive as first impressions may indicate. In fact, many studies show that it is not the willingness or ability to improve, but the time required that is often the problem.

Four main goals of process improvement are:

- Cutting costs

- Cutting waste

- Improving quality

- Removing stress

Two popular ways of improving processes are benchmarking and waste identification. Either way, it's all about removing things that do not add value and adding more value where it is needed.

Benchmarking is all about using metrics to grade a process. These grades can then be compared to either other internal benchmark grades or external benchmark grades dealing with similar processes. Internal comparisons are used for continuous improvement from where the company was previously at. External comparisons are used to find out how well a process compares to the best versions of those processes on a local, national, or even global scale.

Benchmarking and process improvement is comprised of the following steps:

- Talk to those dealing with the process (to gain information and buy-in)

- Create metrics for comparing improvement levels

- Collect metrics before a change (as the process exists today)

- Make the change

- Collect metrics after a change

- Make sure the improvements and measurements are statistically significant

- Present findings, real world benefits, and recommendations

- Officially incorporate the changes into the process

- When needed, benchmark again for continued improvement

- Time

- Number of people involved

- Number of manual steps

- Number of communication methods or problems

- Amount of redundancy

- Transportation (moving things more than needed)

- Inventory (any unneeded storage or depreciation)

- Motion (people moving more than needed)

- Waiting

- Over production (making more than needed)

- Over processing (poor tool use)

- Defects (taking extra time to find defects and fix them)

- Underutilized resources

- Process Diagrams & Value Stream Mapping

- Cause and Effect (also known as either Fishbone or Ishikawa diagrams)

- Pareto Charts / Analysis

Cause and Effect diagrams are useful for finding root causes to problems. Looking at the following diagram, you can see why some people call it a fishbone diagram. Every time there is a reason for the effect, an attempt is made to find a lower level cause.

Pareto charts are cross plots of specific problem types vs total problems (relative vs. absolute). They are useful in showing which problem areas should be addressed first.

If it is uncertain whether a process needs to be benchmarked or improved, try looking at that process from a customer's perspective and see if you would be impressed or left wanting.

Strategy Performance 07 December, 2010

After strategies have been created and a direction has been set, a company must perform well to see the desired results. One popular way to measure strategy performance is by using a Balanced Scorecard (BSC).

The BSC was popularized by Robert Kaplan and David Nortan in 1992. It is similar to a dashboard, but with a focus on company and consumer trade-offs. Stress is placed on an informing purpose rather than a controlling one. It can be thought of as a way to measure strategy because it links a company's actions to its mission and vision.

Balanced Scorecards are created based on four quadrants:

Each of these quadrants are further broken down into:

Goals should be specific, but cover many parts of each quadrant such as:

There are many benefits to the BSC which include:

The BSC was popularized by Robert Kaplan and David Nortan in 1992. It is similar to a dashboard, but with a focus on company and consumer trade-offs. Stress is placed on an informing purpose rather than a controlling one. It can be thought of as a way to measure strategy because it links a company's actions to its mission and vision.

Balanced Scorecards are created based on four quadrants:

- Internal Processes (how efficient are you at satisfying customers?)

- Customers (how do customers see you?)

- Finances (how do shareholders see you?)

- Internal Learning and Innovation (how can you create more value?)

Each of these quadrants are further broken down into:

- Goals

- Measurements

Goals should be specific, but cover many parts of each quadrant such as:

- Short/Long Term

- Financial/Non-Financial

- Leading/Lagging Indicators

- Internal/External Indicators

The following flow shows how the BSC connects strategy to action.

There are many benefits to the BSC which include:

- Showing the impact one change has on other quadrants

- The ability to measure intangible assets

- People are pulled towards the company mission and vision

- Areas that seem disjoint, but are linked, are identified

- Everyone in the company is involved

- Cause and effect relationships between BSC goals and outcomes are identified

- It shows which changes are reflected in the bottom line

- Goals should always be linked to the strategy

- Cause and effect relationships between goals and outcomes should be validated

- Measurements must be valid and statistically significant

- The goals should be communicated throughout the entire company

- Time should be taken to understand how quadrants and quadrant goals are related

Outlining the Marketing Plan 26 August, 2010

Here's an outline for a marketing plan.

Some parts will be longer, others may only be a sentence or even be non-existent.

It's better to avoid 'I', 'we', and 'you', but if you find yourself frustrated or stumbling on these aspects, drop them in favor of smoothness. The meat of the plan and the part that will be of interest to most people will be that of section 'I', which may be the majority of the summary in section 'A'. The rest of the plan is backing, justification, and proof that section 'I' will succeed. Section 'I' explains the actual product, as well as the major assumptions.

A - Executive Summary

1 - State the product, it’s name, the company name, and who your market is

2 - Give a brief overview of the whole plan

a - Summarize assessments

b - Summarize goals

c - Summarize recommendations

B - Introduction

C - Customer Analysis

1 - Customer identification/definition

2 - Customer demographics, needs assessment, and decision-making

a - Detail the market vs general target segments

b - Describe Industry worth

c - How many potential customers are there?

d - How is the potential customer base changing?

e - Explain the target customers’ demographics

f - Detail the target customers’ psychographics

g - Detail the target customers’ geographics

h - Detail the needs of the target customers

i - Detail the drivers of the customers’ decision-making

j - What will make consumers choose this product

k - Are the target market’s decisions influenced by others

l - What impact will the product have on the target market

m - How much education & change will need to take place

n - Detail customers’ price and augmented product’s preferences

o - Detail service required

3 - Comprehensive profiles of a company’s target customers

4 - Detail any partners and partner’s decision making process or show there are none

D - Current marketing Situation Analysis

1 - Market overview/brief description & the company’s place in the market

2 - Product line overview

a - What other products does the company have?

b - Where does the new product fit into the existing line?

3 - External Analysis (SLEPT/Partial Porters)

a - Social (trends & their effects)

b - Legal (regulations, labor unions)

c - Economic

i - supply, demand, equilibrium

ii - vulnerability to preference changes

iii - fiscal, monetary, inflation, unemployment

d - Political (federal, local, favor of political party to industry, political changes)

e - Technological

i - evolution, choices available

ii - technological leads, innovation, can we keep up?

f - Industry

i - Show the leader in the market

ii - Show recent changes in power/trends in competition

g - Customers

i - How are demands changing over time?

ii - Is the company or consumer in power?

h - Suppliers

i - Show partners/value adding groups

ii - Is the company or supplier in power?

i - New industry entrants

i - How are the barriers to entry?

ii - Are there many new entrants?

4 - Internal Analysis

a - Resourced based view

b - Functional view

c - Value-chain

d - Competency matrix

e - Building blocks of competitive advantage

E - SWOT

F - Competitive Analysis

1 - Define what kinds of competition exist

a - Substitutes (direct)

b - In house or other (indirect)

2 - Describe competitors and show competitive advantage

a - Define each direct competitor individually

i - Strengths

ii - Weaknesses

iii - How do they satisfy the target market’s needs?

b - Group and categorize each major competitor

c - Describe the company’s competitive advantages

i - Efficiency

ii - Quality

iii - Innovation

iv - Responsiveness to customers

v - Providing incentives

vi - Access to limited or exclusive resources

G - Distribution overview

1 - Describe existing distribution channels and their effectiveness

2 - Describe trends in sales of similar products

3 - Overview of if the product will be sold in similar fashion to others

4 - Ordering

H - Place in the market

1 - Overview of company strategy

2 - List goals

3 - Issues affecting goal accomplishment

I - Marketing Strategy (What do to based on what was already stated/How to do it)

1 - Value Proposition/Product

a - Describe the core product

b - Describe the augmented product

c - What need will it satisfy

d - Why will a consumer choose this product?

e - Evolution of the product/it's successors

2 - Segmentation

a - Describe your market and detail how you will segment it

b - Justify why the market will be segmented in this way

c - Describe the segmentation variables and the segment’s differences

d - Describe why other segments are not being targeted

3 - The Rest of the Marketing mix

a - Price

i - Value of new offering

ii - Difference between new offering and what exists

iii - Pricing strategy

b - Place/distribution

i - Sales plan

ii - Sales forecast

c - Promotion

i - Acquiring customers

ii - Retaining customers

iii - Education

iv - Facts

4 - Marketing research needed

5 - Time Lines

J - Action & Control

1 - Action Program

a - List the first year’s initiatives

b - Estimate at what time each will be done in relation to other things

c - Estimate how long they will take

2 - Controls

a - What checkpoints are necessary to make sure everything is on track?

b - How will changes in the environment be handled?

c - What will be measured?

K - Conclusion

Some parts will be longer, others may only be a sentence or even be non-existent.

It's better to avoid 'I', 'we', and 'you', but if you find yourself frustrated or stumbling on these aspects, drop them in favor of smoothness. The meat of the plan and the part that will be of interest to most people will be that of section 'I', which may be the majority of the summary in section 'A'. The rest of the plan is backing, justification, and proof that section 'I' will succeed. Section 'I' explains the actual product, as well as the major assumptions.

A - Executive Summary

1 - State the product, it’s name, the company name, and who your market is

2 - Give a brief overview of the whole plan

a - Summarize assessments

b - Summarize goals

c - Summarize recommendations

B - Introduction

C - Customer Analysis

1 - Customer identification/definition

2 - Customer demographics, needs assessment, and decision-making

a - Detail the market vs general target segments

b - Describe Industry worth

c - How many potential customers are there?

d - How is the potential customer base changing?

e - Explain the target customers’ demographics

f - Detail the target customers’ psychographics

g - Detail the target customers’ geographics

h - Detail the needs of the target customers

i - Detail the drivers of the customers’ decision-making

j - What will make consumers choose this product

k - Are the target market’s decisions influenced by others

l - What impact will the product have on the target market

m - How much education & change will need to take place

n - Detail customers’ price and augmented product’s preferences

o - Detail service required

3 - Comprehensive profiles of a company’s target customers

4 - Detail any partners and partner’s decision making process or show there are none

D - Current marketing Situation Analysis

1 - Market overview/brief description & the company’s place in the market

2 - Product line overview

a - What other products does the company have?

b - Where does the new product fit into the existing line?

3 - External Analysis (SLEPT/Partial Porters)

a - Social (trends & their effects)

b - Legal (regulations, labor unions)

c - Economic

i - supply, demand, equilibrium

ii - vulnerability to preference changes

iii - fiscal, monetary, inflation, unemployment

d - Political (federal, local, favor of political party to industry, political changes)

e - Technological

i - evolution, choices available

ii - technological leads, innovation, can we keep up?

f - Industry

i - Show the leader in the market

ii - Show recent changes in power/trends in competition

g - Customers

i - How are demands changing over time?

ii - Is the company or consumer in power?

h - Suppliers

i - Show partners/value adding groups

ii - Is the company or supplier in power?

i - New industry entrants

i - How are the barriers to entry?

ii - Are there many new entrants?

4 - Internal Analysis

a - Resourced based view

b - Functional view

c - Value-chain

d - Competency matrix

e - Building blocks of competitive advantage

E - SWOT

F - Competitive Analysis

1 - Define what kinds of competition exist

a - Substitutes (direct)

b - In house or other (indirect)

2 - Describe competitors and show competitive advantage

a - Define each direct competitor individually

i - Strengths

ii - Weaknesses

iii - How do they satisfy the target market’s needs?

b - Group and categorize each major competitor

c - Describe the company’s competitive advantages

i - Efficiency

ii - Quality

iii - Innovation

iv - Responsiveness to customers

v - Providing incentives

vi - Access to limited or exclusive resources

G - Distribution overview

1 - Describe existing distribution channels and their effectiveness

2 - Describe trends in sales of similar products

3 - Overview of if the product will be sold in similar fashion to others

4 - Ordering

H - Place in the market

1 - Overview of company strategy

2 - List goals

3 - Issues affecting goal accomplishment

I - Marketing Strategy (What do to based on what was already stated/How to do it)

1 - Value Proposition/Product

a - Describe the core product

b - Describe the augmented product

c - What need will it satisfy

d - Why will a consumer choose this product?

e - Evolution of the product/it's successors

2 - Segmentation

a - Describe your market and detail how you will segment it

b - Justify why the market will be segmented in this way

c - Describe the segmentation variables and the segment’s differences

d - Describe why other segments are not being targeted

3 - The Rest of the Marketing mix

a - Price

i - Value of new offering

ii - Difference between new offering and what exists

iii - Pricing strategy

b - Place/distribution

i - Sales plan

ii - Sales forecast

c - Promotion

i - Acquiring customers

ii - Retaining customers

iii - Education

iv - Facts

4 - Marketing research needed

5 - Time Lines

J - Action & Control

1 - Action Program

a - List the first year’s initiatives

b - Estimate at what time each will be done in relation to other things

c - Estimate how long they will take

2 - Controls

a - What checkpoints are necessary to make sure everything is on track?

b - How will changes in the environment be handled?

c - What will be measured?

K - Conclusion

Brand: It's All In Your Head 16 July, 2010

A company's brand is simply what a consumer thinks of a company and it's products. It represents a set of promises that a company makes to a consumer.

Brand equity consists of assets and liabilities linked to a brand that change the value of a product. It can also be thought of as the value of the company if the firm's total asset value was subtracted from the firms estimated value.

Building a brand can trump everything else in marketing, for better or for worse. Brands have the ability to create customer loyalty, lower competition, create larger margins, lower price sensitivity of products, create greater trade, create better communication effectiveness, and create brand extension opportunities.

The key to branding: The power of a brand is in the mind of the consumer

From a practical standpoint, consumers will rate a brand based on three things:

1 - The expertise of the company

2 - The similarity of products produced

3 - The absence of brand extension exploitation

Many characteristics and features that augment a product, such as warranty time, can affect branding. Popular culture, influencers, customers, and the firm can influence the culture or story behind a brand.

The value of a brand can be measured in four parts:

1 - Reputation

2 - Relationship

3 - Experience

4 - Symbolism

The Young and Rubicam Group have four ideas that when measured, can determine the health of a brand:

1 - Differentiation

2 - Relevance

3 - Esteem

4 - Knowledge

When differentiation is greater than relevance, the brand can grow. Otherwise, it cannot. When esteem is greater than knowledge, the customer will want a closer relationship. Otherwise, it will not. Brand strength is the combination of differentiation and relevance. Brand stature is the combination of esteem and knowledge.

Kevin Keller developed a model called the Customer Based Brand Equity (CBBE) Pyramid. It has the goal of allowing a company to:

1 - Decide what the brand should mean

2 - Develop a link between the brand and the product

3 - Get positive reactions

4 - Build lasting customer relationships

Brand equity consists of assets and liabilities linked to a brand that change the value of a product. It can also be thought of as the value of the company if the firm's total asset value was subtracted from the firms estimated value.

Building a brand can trump everything else in marketing, for better or for worse. Brands have the ability to create customer loyalty, lower competition, create larger margins, lower price sensitivity of products, create greater trade, create better communication effectiveness, and create brand extension opportunities.

The key to branding: The power of a brand is in the mind of the consumer

From a practical standpoint, consumers will rate a brand based on three things:

1 - The expertise of the company

2 - The similarity of products produced

3 - The absence of brand extension exploitation

Many characteristics and features that augment a product, such as warranty time, can affect branding. Popular culture, influencers, customers, and the firm can influence the culture or story behind a brand.

The value of a brand can be measured in four parts:

1 - Reputation

2 - Relationship

3 - Experience

4 - Symbolism

The Young and Rubicam Group have four ideas that when measured, can determine the health of a brand:

1 - Differentiation

2 - Relevance

3 - Esteem

4 - Knowledge

When differentiation is greater than relevance, the brand can grow. Otherwise, it cannot. When esteem is greater than knowledge, the customer will want a closer relationship. Otherwise, it will not. Brand strength is the combination of differentiation and relevance. Brand stature is the combination of esteem and knowledge.

Kevin Keller developed a model called the Customer Based Brand Equity (CBBE) Pyramid. It has the goal of allowing a company to:

1 - Decide what the brand should mean

2 - Develop a link between the brand and the product

3 - Get positive reactions

4 - Build lasting customer relationships

Figure 1 - CBBE Pyramid

The definitions that follow describe the CBBE pyramid, and can be though of in terms of understanding nomenclature. To communicate an idea, sometimes certain words or phrases are used, and in the beginning, synonyms are the only way a person has of understanding what the initial words or phrases mean. The following definitions will be defined by their synonyms because it seems this is the most effective way to talk about these brand ideas.

Brand Salience - Identity & awareness. It shows what basic functions the brand provides. It also allows the consumer to see new usage situations that were previously ignored or forgotten.

Brand Performance & Imagery - Meaning & associations. Performance is all about functional needs. This includes quality, utility, asthetics, and economic needs. It includes primary and secondary functions as well as reliability, servicability (effectiveness, efficiency, and empathy), and durability. It also includes style, design, and price.

Imagery is all about psychological and social needs. It is about user profiles, purchase scenarios, usage scenarios, personality, values, history, heritage, and experiences.

Both Performance and imagery can be profiled by looking at three main categories: Strength, Favorability, and Uniquness in that order.

Consumer Judgements & Feelings - The effects that the knowledge and product a company publicizes has on consumers. Quality, credibility, consideration, and superiority are judgement attributes. Warmth, fun, excitement, security, social approval, and self-respect are feeling attributes.

Consumer Brand Resonance - Brand loyalty. This means behavior loyalty, bonding attitudes, a sense of community, and active engagement.

A consumer cannot have brand loyalty to all the brands they come in contact with. This is due to both conflicting allegiances and personal differences and preferences. This links nicely with Jennifer Aaker's theory on brand personality. The theory states that if people choose friends based on personality, they should be able to choose products and services based on some similar personality. Doing this generally involves surveys that ask questions falling into the following categories (thus showing a product's personality) :

1 - Sincerity

2 - Excitement

3 - Competence

4 - Sophistication

5 - Ruggedness

Another method used in gaining consumer insights is the ZMET (Zaltman Metaphor Elicitation Technique). This method has a consumer gather images about a brand or product, and then use those images to tell a story. Missed images, sensory images, and image groups are also discussed. This method's main benefit is removing the constraints on voice/language and the asking of specific questions in gaining insights. It helps consumers say what they want to without putting their ideas into words.

The Link Between Consumers and Brands - A brand should help a consumer remember and understand the differences between a competitors brand and your brand.

Brands should:

- Suggest something about the product's benefits and qualities

- Be easy to pronounce recognize and remember

- Be distinctive

- Be extensible

- Translate into foreign languages

- Be capable of registration and legal protection

Brands must continually be built even if they are already strong. Competitive and consumer shifts can occur, and change everything. The time it takes to build a brand will be proportional to the time it takes to create enough awareness and understanding with consumers. In the end, it's what the consumer thinks that makes or breaks a firm.

Marketing and the Yardstick 15 July, 2010

Why should anyone measure marketing? The 'why measure' answer is pretty obvious, but the fact that marketing is being measured is interesting. Marketing costs a lot. Brand health + marketing = the company's reputation. Finally, the customer is usually the source of all cash for the company.

It's important to ask how the customer's needs are changing, how the firm can be loyal to the customer, and how marketing effectiveness can be measured in terms of the bottom line.

One way to create and understand measurements is by using a dashboard. A dashboard is simply a set of indicators that can be glanced at and absorbed quickly. There are several points to be made when talking about dashboards. Not a lot of explanation is needed. Use the following list as a dashboard creation guide, and the result will be above average.

- Don't overload it with too much information.

- Include operational, financial, customer, and quality metrics.

- Include driver, pipeline, resource, and talent information.

- Include innovation information.

- Show how the entire company as a whole is doing.

- Visualizations should be simple and easy to digest.

- Use a combination of historical data and leading indicators.

- Focus on leading indicators.

- Metrics should be as real time as possible.

- Only show controllable metrics.

- Use baselines to allow the flagging of extraordinary results.

- Echo corporate strategy in the metrics.

- Measure short and long term goal metrics.

- Create standard definitions for metrics.

- Verify metrics are absolutely correct.

- Allow for an audit trail to see the details.

- Casual (cause and effect) measurements should be used.

- Verify that the metrics matter.

- Measurement methods must be consistent across the company.

- Results should be shared.

- Results should be acted upon.

- Metrics should expose inadequacies.

There's the list.

A Smattering Description of 'Promotion' (IMC)

Marketing promotion/communications (often called Integrated Marketing Communications or IMC) can have several forms. Advertising, PR, value chain discounts, sales promotions, personal selling, in store displays and kiosks, direct marketing, and samples are some examples of IMC. This is really where marketing affecting consumers. Consumers must know about a product before they decide to purchase it. Push strategies attempt to keep contacting a consumer in hopes that they will buy the product. Pull strategies are focused on creating enough demand that consumers purchase a product with out being reminded to do so.

Public relations (PR) includes marketing communications and promotion by means of press releases, speeches, and service activities. While this can be a great and cheap way of gaining publicity, there is no guarantee that the publicity will be good. News agencies are entitled to interpret and show PR as they deem fit.

It is important to remember that when thinking about marketing communications, advertising should usually win out over promotions. Promotions will create a lift over the usual baseline profits, but this is generally short lived. Given price fluctuations that promotions create, the price sensitivity of a product goes up and the price premium that a brand can command will decrease.

While promotions can bring in extra money, they are usually thought of as short term solutions. Advertising products or a brand is thought of as a long term solution. The profits from advertising may not be as evident as in promotions, but it does lead a firm down the path of long term success.

The biggest hurdles to cross when advertising are identifying the target audience. After this has been done it is necessary to inform them, give them a trial experience, or get them to repurchase a product. The final step is creating the advertisement. This is usually done with one of the following goals:

- Educating consumers (product purpose and differentiation)

- Appealing to humor

- Appealing to fears

- Adding a belief to a consumer's mindset

- Conditioning

- Repetition

- Endorsements

Adding beliefs are important because it can be counter productive to attempt to change a person's beliefs.

It's also important to not forget the power of buzz and communities. They can alter the perception and hype of a product immensely.

Although IMC is one of the original 4 parts of the marketing mix and can sometimes include both promotion and placement, many companies will outsource it to avoid becoming an advertising agency themselves.

A Smattering Description of 'Price'

Price is some compensation that is exchanged by two parties. In internal business, it's all about the price.

Aside from price being a factor of purchase, there are several other functions it serves. Determining profits, sales, market share, and store traffic are a few. It creates a perception of quality or exclusiveness. It can encourage trials, and discourage competition.

There are several pricing strategies that should be considered when pricing products. These will be given in a list form because there are so many.

Cost-Plus Pricing: The cost of a product + a percent markup. This strategy ignores many environmental factors, but guarantees profits if sales are made.

Price Skimming: The price is initially set high to gain extra profits from early adopters, but set lower as more competition enters. This can work, but invites competition.

Penetration Pricing: The start cost is lower to help enter the market. Most profits are made by not raising the price, but by cutting costs.

Prestige Pricing: Creating a perception in the consumer's mind that quality is high, and they must pay a higher price for the product.

Bait and Hook: The initial price of the main product is low, but replacement parts and other materials or services consumed in the process have higher prices. This works unless a competitor can create low priced replacement parts and materials.

Price Promotions: This can be used to introduce new products or prevent consumers from defecting. It is also effective in selling older products when newer ones are available. Too many price promotions can cause consumers to wait and only purchase when there is a promotion, or switch between brands, cycling through promotions.

According to Robert Dolan's true economic value (TEV) theory, consumers are only willing to pay the cost of the best alternative + the value of the performance difference. This can be useful in setting an initial price for a product based on what consumers are currently buying. When setting initial prices, it is important to be clear on what market segment is being targeted.

Companies must revisit pricing strategies often and make sure they correspond to where the product is in the product life-cycle.

The Strategic Pricing Group created a pyramid that can be used as a framework to not only set a price for a product, but to have resources and a company capable of backing that price up.

1 - Value Creation: A product must be created and priced so a customer will pay for it, not simply be satisfied by it.

2 - Price Structure: Pricing should be based on the value received instead of the product delivered. Price for a customer segment rather than a product.

3 - Price and Value Communication: When value is not communicated, the doors to price sensitivity and price negotiations open. This becomes problematic. Having a communications strategy that uses both performance facts as well as psychological benefits will help solidify a value to a consumer.

4 - Pricing Policy: A stance must be taken on the frequency of discounts and promotions given. If this is not done, the customer base will drive profits down faster than the general efficient market.

5 - Price Level: Actual prices must be set and periodically reviewed in the same way throughout the company. This can take the form of a planned decision model that uses relevant data about how the market will respond to changes. Many times the best model is simply a fixed price/variable offering one.

These 5 steps should be consistently known throughout the organization.

What has been stated up until now has largely been academic in nature. It is now necessary to turn attention to a customer's view of their willingness to buy.

Consumers will buy a product based on:

1 - When its perceived value exceeds its price.

2 - Fairness compared to another consumer's purchase or a producer's cost.

3 - Incentives relative to the price.

4 - Reference prices such as the last known sale or purchase price.

5 - Perceived exploitation of the consumer.

Consumers will remain customers if they know there is value in the product. Remembering that a product has value includes:

1 - Actually using a previously purchased product.

2 - Understanding per line item if there are parts, what the cost is.

3 - Paying for the product close to the time of use, which enforces the product's value.

Pricing can make or break a product line even if the products are great. These steps will help act as a guide, making sure the price matches not only the product, but the market.

Aside from price being a factor of purchase, there are several other functions it serves. Determining profits, sales, market share, and store traffic are a few. It creates a perception of quality or exclusiveness. It can encourage trials, and discourage competition.

There are several pricing strategies that should be considered when pricing products. These will be given in a list form because there are so many.

Cost-Plus Pricing: The cost of a product + a percent markup. This strategy ignores many environmental factors, but guarantees profits if sales are made.

Price Skimming: The price is initially set high to gain extra profits from early adopters, but set lower as more competition enters. This can work, but invites competition.

Penetration Pricing: The start cost is lower to help enter the market. Most profits are made by not raising the price, but by cutting costs.

Prestige Pricing: Creating a perception in the consumer's mind that quality is high, and they must pay a higher price for the product.

Bait and Hook: The initial price of the main product is low, but replacement parts and other materials or services consumed in the process have higher prices. This works unless a competitor can create low priced replacement parts and materials.

Price Promotions: This can be used to introduce new products or prevent consumers from defecting. It is also effective in selling older products when newer ones are available. Too many price promotions can cause consumers to wait and only purchase when there is a promotion, or switch between brands, cycling through promotions.

According to Robert Dolan's true economic value (TEV) theory, consumers are only willing to pay the cost of the best alternative + the value of the performance difference. This can be useful in setting an initial price for a product based on what consumers are currently buying. When setting initial prices, it is important to be clear on what market segment is being targeted.

Companies must revisit pricing strategies often and make sure they correspond to where the product is in the product life-cycle.

The Strategic Pricing Group created a pyramid that can be used as a framework to not only set a price for a product, but to have resources and a company capable of backing that price up.

Figure 1 - The Strategic Pricing Pyramid

1 - Value Creation: A product must be created and priced so a customer will pay for it, not simply be satisfied by it.

2 - Price Structure: Pricing should be based on the value received instead of the product delivered. Price for a customer segment rather than a product.

3 - Price and Value Communication: When value is not communicated, the doors to price sensitivity and price negotiations open. This becomes problematic. Having a communications strategy that uses both performance facts as well as psychological benefits will help solidify a value to a consumer.

4 - Pricing Policy: A stance must be taken on the frequency of discounts and promotions given. If this is not done, the customer base will drive profits down faster than the general efficient market.

5 - Price Level: Actual prices must be set and periodically reviewed in the same way throughout the company. This can take the form of a planned decision model that uses relevant data about how the market will respond to changes. Many times the best model is simply a fixed price/variable offering one.

These 5 steps should be consistently known throughout the organization.

What has been stated up until now has largely been academic in nature. It is now necessary to turn attention to a customer's view of their willingness to buy.

Consumers will buy a product based on:

1 - When its perceived value exceeds its price.

2 - Fairness compared to another consumer's purchase or a producer's cost.

3 - Incentives relative to the price.

4 - Reference prices such as the last known sale or purchase price.

5 - Perceived exploitation of the consumer.

Consumers will remain customers if they know there is value in the product. Remembering that a product has value includes:

1 - Actually using a previously purchased product.

2 - Understanding per line item if there are parts, what the cost is.

3 - Paying for the product close to the time of use, which enforces the product's value.

Pricing can make or break a product line even if the products are great. These steps will help act as a guide, making sure the price matches not only the product, but the market.

A Smattering Description of 'Product' 14 July, 2010

Products can often be though of as bundles of consumer benefits. The core benefit is really what the consumer is buying. Products can be end results. They can be services or physical objects. According to Michael Solomon, they can even be people, places, and ideas.

Products are an interesting part of the marketing mix (product, price, promotion, and sometimes placement) because products are the most difficult to change after they have been planned and manufactured.

Products have elements of convenience, shopping, specialty, low & high involvement, function, and emotion. It is important to market these factors correctly because by default, not everyone will place a product in the same categories.

Brand, delivery, installation, customer service, warranties, and payment methods are some examples of how a product can be augmented. As a product becomes more mainstream, augmentation will become more important as a differentiator.

The speed of adoption is critical when computing the time at which a product's/product mix's income will have passed development costs and surface as profit. Rogers created the ACCORD acronym to show influencers of adoption:

A - Advantage (superiority)

C - Compatibility (with the consumer)

C - Complexity (understandability and use)

O - Observability (of adoption by others)

R - Riskiness (consequences of adoption)

D - Divisibility (gradual adoption)

There are several attributes used to describe a product line. These attributes can help a marketer decide how to communicate differences from one product to another:

Breadth: Number of product lines.

Depth, Length: Number of products within a line.

Horizontal dimension: Differentiation by consumer taste.

Vertical dimension: Differentiation by performance and price.

Continuous innovation: An improvement to how something is currently done.

Discontinuous innovation: A new way of doing something.

First you generate ideas. After amassing a number of ideas, those ideas are screened. The ideas that remain are fleshed out into concepts. When you have screened concepts, it is a good time to start getting market feedback. With that feedback in mind, a marketing strategy is defined and a business case is built for a rough idea of whether or not the concept is profitable. Product development then begins. Depending on the cost of product development, an amount of test marketing takes place during the product development. Finally, commercialization occurs and the product is released.

A process for product development:

Two parts to the above list may not be obvious at first:

Go/No-Go decisions must not be based on passing simple hurdles, some metrics may be needed.

Also, the product must fit the company and it's mission.

Consumers will compare products to competing products. If no competition for a product exists, consumers will compare the new product to the current way of doing things without the new product.

In theory, product life-cycles generally follow a development, introduction, growth, maturity, and decline stage.

In practice they fluctuate based on fads, urgent needs, competition, education about the product, and abstract or paradigm shifting products. In fact, Frank Bass created an abstract model that can give an idea of product demand and sales to interested parties:

At the end of the day, some products may have little demand. Even those products with little demand should be maintained as long as they bring in enough to cover their costs. This is done to placate consumers who have already purchased older products and may feel like they have been abandoned or that what they have is obsolete if the product is discontinued. Then again, maybe that's the marketing spin you want.

Products are an interesting part of the marketing mix (product, price, promotion, and sometimes placement) because products are the most difficult to change after they have been planned and manufactured.

Products have elements of convenience, shopping, specialty, low & high involvement, function, and emotion. It is important to market these factors correctly because by default, not everyone will place a product in the same categories.

Brand, delivery, installation, customer service, warranties, and payment methods are some examples of how a product can be augmented. As a product becomes more mainstream, augmentation will become more important as a differentiator.

The Product Mix

A product mix is made up of all product lines. A product line is a number of products that have a similar function, style, manufacturing process, distribution process, consumption method, or market segment. These exist so a firm can satisfy multiple market segments at once.The speed of adoption is critical when computing the time at which a product's/product mix's income will have passed development costs and surface as profit. Rogers created the ACCORD acronym to show influencers of adoption:

A - Advantage (superiority)

C - Compatibility (with the consumer)

C - Complexity (understandability and use)

O - Observability (of adoption by others)

R - Riskiness (consequences of adoption)

D - Divisibility (gradual adoption)

There are several attributes used to describe a product line. These attributes can help a marketer decide how to communicate differences from one product to another:

Breadth: Number of product lines.

Depth, Length: Number of products within a line.

Horizontal dimension: Differentiation by consumer taste.

Vertical dimension: Differentiation by performance and price.

Continuous innovation: An improvement to how something is currently done.

Discontinuous innovation: A new way of doing something.

New Product Development

New product development should always be taking place. Although many innovations become apparent after consumers are exposed to them, innovations and products alone cannot create demand. Consumers must want or need a product once it exists.First you generate ideas. After amassing a number of ideas, those ideas are screened. The ideas that remain are fleshed out into concepts. When you have screened concepts, it is a good time to start getting market feedback. With that feedback in mind, a marketing strategy is defined and a business case is built for a rough idea of whether or not the concept is profitable. Product development then begins. Depending on the cost of product development, an amount of test marketing takes place during the product development. Finally, commercialization occurs and the product is released.

A process for product development:

- Observe the situations of consumers

- Generate ideas

- Screen concepts

- Research concept components

- Create go/no-go decision points

- Analyze the product's business model

- Prototype

- Test the market

- Promote/Distribute

Two parts to the above list may not be obvious at first:

Go/No-Go decisions must not be based on passing simple hurdles, some metrics may be needed.

Also, the product must fit the company and it's mission.

Consumers will compare products to competing products. If no competition for a product exists, consumers will compare the new product to the current way of doing things without the new product.

In theory, product life-cycles generally follow a development, introduction, growth, maturity, and decline stage.

In practice they fluctuate based on fads, urgent needs, competition, education about the product, and abstract or paradigm shifting products. In fact, Frank Bass created an abstract model that can give an idea of product demand and sales to interested parties:

| a | = | Consumers making up their minds independently |

| b | = | Consumers who act on word of mouth |

| Bt | = | Consumers to date who purchased the product |

| M | = | All consumers in the Product's market |

At the end of the day, some products may have little demand. Even those products with little demand should be maintained as long as they bring in enough to cover their costs. This is done to placate consumers who have already purchased older products and may feel like they have been abandoned or that what they have is obsolete if the product is discontinued. Then again, maybe that's the marketing spin you want.

Decisions, Decisions, Decisions 13 July, 2010

Decisions are made by people all day, and every day. A key question for marketers then becomes "How can we influence those decisions in our favor?" Interestingly, the answer is more defined than one might think. There is a pattern that most people follow when making decisions. The steps are outlined below.

1. Problem recognition - This is caused by seeing a difference in reality and ideal. A marketing message can cause a customer to recognize this difference.

2. Information search - Consumers identify solutions based on memories or the external environment. Marketing communicates information about products in hopes of leaving the consumer with good memories of it's product.

3. Evaluation of alternatives - Consumers narrow down solutions based on what they like, as well as what is feasible. Marketing attempts to get consumers to use evaluative criteria that is in their favor.

4. Product choice - Consumers use heuristics to make a final decision. Marketing attempts to communicate which heuristics are important. Examples are price equals quality, brand loyalty, and country of origin matters.

5. Post-purchase evaluation - Consumers decide if the decision they made was a good one. They compare what they received with a standard of what they thought they would receive. This has a large effect on how the consumer perceives that company, along with the company's brand and products.

Consumer's decisions in this model can be influenced by a number of factors.

1. Perception: Exposure, Attention, and Interpretation of marketing and critic messages.

2. Learning: Associating similar products, having consequences, receiving bundled stimulus, and observing others.

3. Motivation: Consumers divide needs into categories based on Maslow's hierarchy of needs (survival, safety, belonging, confidence, self-fulfillment). Originally it was thought that a lower level needed to be satisfied before higher levels, but in practice this is not always the case.

Personality traits also affect decisions:

Having the desire to try new things, own products, interact socially, and think about things affect what a consumer buys. Self confidence is also a big personality determinant.

Age, family life cycle, psychographics (grouping people depending on activities, interests, and opinions [AIOs]), arousal, pleasure, time, culture, social class, group think, opinion leaders, sex roles, and product communities all influence a consumer's decisions.

Another determinant is self concept. Self concept is the set of beliefs a person holds about themselves (attributes and abilities). People may have different self concepts at different times depending on what situation they are in and who they are with. This is important because it means that marketing must make sure the correct self concept is active when marketing communications are made.

The ideal self seems to be more influential than the actual self when dealing with social products. When dealing with functional products, actual self seems to take precedence.

This model is indeed more structured that meets the eye, and marketers can use it to their advantage.

1. Problem recognition - This is caused by seeing a difference in reality and ideal. A marketing message can cause a customer to recognize this difference.

2. Information search - Consumers identify solutions based on memories or the external environment. Marketing communicates information about products in hopes of leaving the consumer with good memories of it's product.

3. Evaluation of alternatives - Consumers narrow down solutions based on what they like, as well as what is feasible. Marketing attempts to get consumers to use evaluative criteria that is in their favor.

4. Product choice - Consumers use heuristics to make a final decision. Marketing attempts to communicate which heuristics are important. Examples are price equals quality, brand loyalty, and country of origin matters.

5. Post-purchase evaluation - Consumers decide if the decision they made was a good one. They compare what they received with a standard of what they thought they would receive. This has a large effect on how the consumer perceives that company, along with the company's brand and products.

Consumer's decisions in this model can be influenced by a number of factors.

1. Perception: Exposure, Attention, and Interpretation of marketing and critic messages.

2. Learning: Associating similar products, having consequences, receiving bundled stimulus, and observing others.

3. Motivation: Consumers divide needs into categories based on Maslow's hierarchy of needs (survival, safety, belonging, confidence, self-fulfillment). Originally it was thought that a lower level needed to be satisfied before higher levels, but in practice this is not always the case.

Figure 1 - Maslow's Hierarchy of Needs

Having the desire to try new things, own products, interact socially, and think about things affect what a consumer buys. Self confidence is also a big personality determinant.

Age, family life cycle, psychographics (grouping people depending on activities, interests, and opinions [AIOs]), arousal, pleasure, time, culture, social class, group think, opinion leaders, sex roles, and product communities all influence a consumer's decisions.

Another determinant is self concept. Self concept is the set of beliefs a person holds about themselves (attributes and abilities). People may have different self concepts at different times depending on what situation they are in and who they are with. This is important because it means that marketing must make sure the correct self concept is active when marketing communications are made.

The ideal self seems to be more influential than the actual self when dealing with social products. When dealing with functional products, actual self seems to take precedence.

This model is indeed more structured that meets the eye, and marketers can use it to their advantage.

Research & Observing Consumers

Observing consumers may be the most important part of marketing there is. Without knowing the consumer, as well as their needs and thoughts, it is impossible to provide for them. It won't matter what price is set or how innovative a product is. It won't matter where it can be found or how it's existence is communicated. If a product does not satisfy a need, it won't be purchased.

Market Demand

To get a better idea of profitability when looking at primary and secondary market research data you can observe the rate of adoption that is commonly associated with industry products:

Calculating demand for market potential and sales estimates can be further refined by using one of the following example methods:

1 - total market demand = number of buyers X quantity purchased b average buyer per year X price of average unit

2 - total number of households in target region X those who can use it X those who can purchase it X etc.

Market Research

Primary data - information gathered for a specific purpose

Secondary data - information previously collected for another purpose

Both primary and secondary data must be relevant, current, accurate, and impartial.

This data can be gathered via numerous methods, most of which are obvious:

observation

survey

experiment

mail telephone

personal

online

sampling group, size, procedure (random, random from split up groups, convenience, judgment, quota)

questionnaire

instruments

There are several ways to observe consumers and collect their thoughts. Interviews, focus groups, surveys, previously created documentation, and simply watching them are the main ways. Each of these methods will work to a degree, but it is usually a time and cost constraint on the observer that limits which methods will be used and to what degree they can be used.

Interviews are usually the best observation method, but also have the highest cost. Surveys are one of the easiest and lowest cost methods, but also one of the least effective. This is because the effectiveness of gaining consumer insights is usually proportional to the relationship that exists between the consumer and the observer. Observers and consumers with stronger relationships tend to have discussions where more is disclosed. More disclosure equates to more completeness. The more experienced the observer is, the less formal and structured the set of questions will be. Usually, it’s considered good practice to ask very open ended questions, funneling down to specific questions only when more detail or clarification is needed. It’s also important to not force the ordering of questions because this invites agendas and can be sensed.

The observer’s job is primarily to listen, but also to record non verbal communication. All verbal communication should be taken care of by an audio recording or video recording if necessary. After the observing process is done, the observer should record their feelings and views. The purpose of consumer observation and interviewing is to generate ideas, check assumptions, form a thesis, find information, and seek opinions. By combining both what is conveyed by those being observed as well as the observer, a more complete picture can be painted.

A few more details about interviews and observing : Watch your own reactions and voice inflections to avoid biasing the interview. Interview 10-15 people; focus groups should be 4-5 for small groups or 6-12 for larger groups. Avoid asking why questions. Address terms of confidentiality and make sure that all the interviewer’s questions are answered. Use an interview discussion guide (IDG). An IDG helps organize topics and provides a funnel mechanism to make sure the interviewer is aware of what general questions should be asked, what specific questions are possible, and what transitions should be used.

As long as you have a good sample size and your sample reflects the needed demographic, following the observation guidelines expressed above will allow you to gain insights that are not only impressive and important, but ones that are correct as well.

Market Demand

To get a better idea of profitability when looking at primary and secondary market research data you can observe the rate of adoption that is commonly associated with industry products:

Calculating demand for market potential and sales estimates can be further refined by using one of the following example methods:

1 - total market demand = number of buyers X quantity purchased b average buyer per year X price of average unit

2 - total number of households in target region X those who can use it X those who can purchase it X etc.

Market Research

Primary data - information gathered for a specific purpose

Secondary data - information previously collected for another purpose

Both primary and secondary data must be relevant, current, accurate, and impartial.

This data can be gathered via numerous methods, most of which are obvious:

observation

survey

experiment

mail telephone

personal

online

sampling group, size, procedure (random, random from split up groups, convenience, judgment, quota)

questionnaire

instruments

There are several ways to observe consumers and collect their thoughts. Interviews, focus groups, surveys, previously created documentation, and simply watching them are the main ways. Each of these methods will work to a degree, but it is usually a time and cost constraint on the observer that limits which methods will be used and to what degree they can be used.

Interviews are usually the best observation method, but also have the highest cost. Surveys are one of the easiest and lowest cost methods, but also one of the least effective. This is because the effectiveness of gaining consumer insights is usually proportional to the relationship that exists between the consumer and the observer. Observers and consumers with stronger relationships tend to have discussions where more is disclosed. More disclosure equates to more completeness. The more experienced the observer is, the less formal and structured the set of questions will be. Usually, it’s considered good practice to ask very open ended questions, funneling down to specific questions only when more detail or clarification is needed. It’s also important to not force the ordering of questions because this invites agendas and can be sensed.

The observer’s job is primarily to listen, but also to record non verbal communication. All verbal communication should be taken care of by an audio recording or video recording if necessary. After the observing process is done, the observer should record their feelings and views. The purpose of consumer observation and interviewing is to generate ideas, check assumptions, form a thesis, find information, and seek opinions. By combining both what is conveyed by those being observed as well as the observer, a more complete picture can be painted.

A few more details about interviews and observing : Watch your own reactions and voice inflections to avoid biasing the interview. Interview 10-15 people; focus groups should be 4-5 for small groups or 6-12 for larger groups. Avoid asking why questions. Address terms of confidentiality and make sure that all the interviewer’s questions are answered. Use an interview discussion guide (IDG). An IDG helps organize topics and provides a funnel mechanism to make sure the interviewer is aware of what general questions should be asked, what specific questions are possible, and what transitions should be used.

Example IDG

As long as you have a good sample size and your sample reflects the needed demographic, following the observation guidelines expressed above will allow you to gain insights that are not only impressive and important, but ones that are correct as well.

The Numbers in a Business Trend 22 June, 2010

Statistics is a subject taught, and usually required in business schools. What’s the reason? It helps us see not only the trends in Business, but what parts of those trends are statistically significant. Regression analysis lets us see what matters in determining costs and prices, and is usually run in conjunction with historical data. In order to explain regression analysis, we need to define a few things:

Median: The middle value in an ordered set of numbers that separates the lower half from the higher half.

Mean: The numeric average of a set of numbers.

Mode: The numeric value in a set of numbers that occurs most frequently.

Variance: The dispersion of numbers in a set around the mean.

Standard Deviation: The variance of a set of numbers whose unit of measurement is the same as those of the number set.

CV (Coefficient of Variation): A ratio of standard deviation to the mean.

R2 (Coefficient of Determination): The ratio of explained variance to total variance.

Standard Error: A measure of fluctuation from one sample statistic to another.

Normal Distribution (standard normal): A bell curved graph used to describe number sets with complete data or a high sample size.

Student’s Distribution (t-distribution): A bell curved graph used to describe number sets when the sample size is small.

Manual Regression: Using a number set to generate a line equation that resembles the trend of the data.

T-Score: An indication of correctness of a hypothesis. This is sometimes called the t-stat.

P-Value: A value that shows the significance of a factor.

Degrees of Freedom: The variability in the curve of a statistic. Generally this equals n-(k+1) where n is the sample size and k is the number of independent variables.

T-Table: A lookup table where one axis represents degrees of freedom and the other axis represents the probability. A T-Score is found where the correct column and row intersect.

Hypothesis Testing: First, you must choose both a hypothesis and an inverse of the hypothesis, such that you can prove one of them by choosing the correct probability when using the T-Table. A null hypothesis (the opposite of what you want to prove) and an alternative hypothesis (what you want to prove) are chosen as equality equations. The equality of the null and alternative hypotheses determines what kind of tail test to use in the lookup table. If the equality symbol used in the alternative hypothesis is a '>', it is a right tailed test. If it is a '<', you have a left-tailed test. If it is neither, you have a two-tailed test. A null hypothesis is generally used for the test because of historical significance in the philosophy of math as well as the innocent until proven guilty axiom.

The following example deals with salaries. If a study claims that programmers make $100,000/year, but you think they make more, H1(The alternative hypothesis) is x > 100,000. The null hypothesis would then be H0(the notation for a null hypothesis): x <= 100,000. The alternative and null hypothesizes are always compliments (opposites) of each other, and the alternative hypothesis (what you are trying to prove) should be stated first.

After comparing data sets using the equations that follow, and comparing the t-stat to the critical value found in the T-Table lookup, we'll have enough information to determine what is correct. Using the standard deviation, t-score, and our data set, we have enough data to make a conclusion.

The significance of the right, left, or two tailed choice is that anything that falls respectively to the right, left or both of the critical regions denoted by the T-Table lookup number equates to rejecting H0, and accepting H1.

Equations:

That's the theory. Most people will simply use Excel or some other program to run all the calculations automatically. However, understanding what is going on, and how to correctly interpret what Excel tells you is much easier if you understand that theory.

Using Excel’s Data Analysis package, you can select columns to include in a regression, at which point you’ll get a nice little table like the following:

So, what does this mean? Well, the point of a regression analysis is to create a fitted line to the scattered data points that we have. The key here is that we want to find a relationship between x (the numbers that drive our end result) and y (our end result) in our plots. The bottom line is: the more significant the variables are, the bigger the slope of the line will be. This also means that the if the relationship is small, the slope of the line will be small. We could say that the closer to 0 the slope is, the less significant that slope is. Because we are trying to prove that something is significant and that the slope is not 0, we can use the following hypothesis. H0: x =0, H1: x!=0, where x is the slope of the regression line. We can take our t-statistic (t) equation from above and see if the slope is statistically significant.

Let's use an example that uses Excel's linear regression to preform a hypothesis test. Using a setup as shown in the screenshot above, Excel gives us a t-stat. We must now use a t-table (google it if you don't have a complete one) to compare the t-stat given by excel to what probability we want. Usually 95% is the standard probability used. Our df (degrees of freedom) is 3. We get this from using the df definition given above, and the data from the screenshot (showing an example of material cost effect on overall cost) : n-(k+1) -> 8-(4+1) -> 3. The T-Table score is 2.353. Excel says our t-stat is .62 for materials. Because .62 is not > 2.353, we do not reject H0, and conclude that the material cost is not significant in the overall cost!

A couple of important notes now that we have seen how hypothesis testing works:- Rejection does not mean something is false, it means that it is not reasonable.

- Accepting does not mean something is true, it means it is reasonable.

- Some people use a p-value rule: Reject H0 if p <>

- Don't just believe the output. Always make sure the numbers make sense.

Presenting on strategy or strategically presenting? 04 May, 2010

Here's a few things I've learned in the last week on presenting.

The executive summary.